The Netherlands is famed for its work-life balance – it’s one of the reasons that so many expats are drawn to this laid-back country and move to the Netherlands to work, even obtaining an orientation year visa to do so. It happens to be one of the most productive countries in the world. When checking your work contract in the Netherlands, it’s good to pay attention to benefits. And one of the most enticing work benefits in the Netherlands is its generous holiday allowance.

What is a holiday allowance?

In the Netherlands, every employee is legally entitled to a holiday allowance – referred to as vakantiegeld in Dutch – on top of their wages. While it’s not the same as a 13th month, it’s roughly equivalent to an extra month’s salary before tax.

Holiday allowance was introduced in the Netherlands around 1910 as a part of collective agreements between industry associations and unions. It was designed to incentivise employees to take a vacation over the summer months and was paid out in May. This way, there was enough time for people to make plans to take a trip between June and September. Due to differences in holiday allowance between industries, the Dutch government introduced legislation in 1968, making it mandatory for all employers to pay a minimum amount, no matter which sector.

There is no obligation to spend the holiday allowance on holidays – employees can spend the money however they wish. Unlike some countries, the Netherlands also requires employers to provide staff with 20 days of paid leave a year, but it’s common practice to provide 25 days of annual paid holiday.

How is the Dutch holiday allowance calculated?

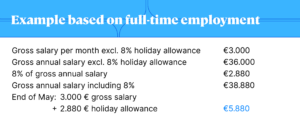

Employees in the Netherlands are required by law to receive at least 8% of their salary as holiday allowance. This also applies to employees with a zero-hours contract. The minimum rate for temporary workers is 8.33%.

Holiday allowance is calculated based on the gross salary of the previous year, including overtime and commission, and is adjusted pro rata: the amount you receive depends on the number of months you have been employed. It does not include bonuses, expenses and profit distribution from shares. Holiday allowance is subject to a special tax rate, just like bonuses and other parts of your salary that you only receive once a year. It’s usually paid out as a lump sum in May or June. Exceptions include when a contract ends or is terminated before May, and when there are alternative arrangements in place: it can also be paid out on a monthly basis and can even be paid out early if agreed in advance.

How can I claim the holiday allowance?

The best part is that you don’t have to do anything to get your holiday allowance. It’s automatically included on your payslip and built up during the employment period from June to May. Each month, you’ll see 8% gross added on top of your salary and it’s generally all paid out at once. This is equivalent to receiving almost one full month of salary (96%) before tax.

While the allowance is adjusted pro-rata, it continues to accumulate as usual while on maternity leave and during sick leave. Partners on parental leave will also receive a reduced amount if they opt to make use of extended partner leave. This involves employees claiming benefits from the Employment Insurance Agency (UWV) for up to 70% of their salary. In most cases, however, you won’t have to do anything in particular in order to claim your holiday allowance, but if you do have questions, contact your company’s HR department for more information.

If you’re interested in finding a job in the Netherlands, check out our vacancies!